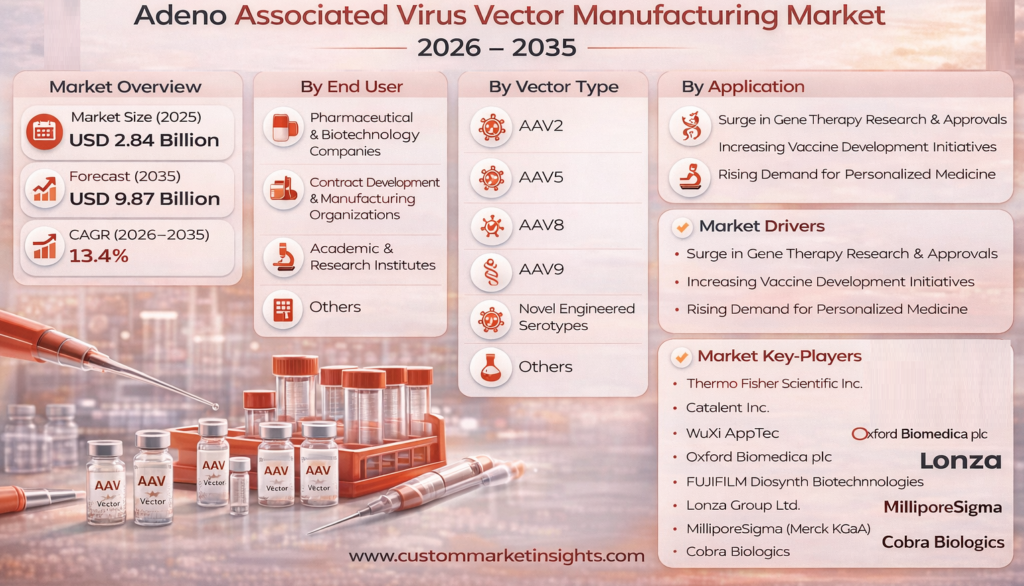

The global Adeno-Associated Virus (AAV) Vector Manufacturing Market is witnessing substantial expansion, fueled by the rapid evolution of gene therapy and increasing demand for advanced biologics. According to recent market estimates, the AAV vector manufacturing market was valued at USD 2.84 billion in 2025 and is expected to grow to USD 3.22 billion in 2026, eventually reaching approximately USD 9.87 billion by 2035, registering a strong CAGR of 13.4% during the forecast period (2026–2035).

AAV vectors have become one of the most widely used delivery systems in gene therapy due to their safety profile, low immunogenicity, and ability to provide long-term gene expression. These vectors play a crucial role in delivering therapeutic genes to target cells, making them highly valuable in treating genetic disorders, rare diseases, and certain chronic conditions.

Market Drivers

The primary driver of the AAV vector manufacturing market is the surge in gene therapy clinical trials and regulatory approvals. Over the past decade, there has been a notable increase in the number of gene therapy programs targeting diseases such as hemophilia, spinal muscular atrophy, and inherited retinal disorders. Regulatory agencies, including the FDA, have accelerated approvals for innovative gene therapies, further boosting demand for AAV vectors.

Another key factor contributing to market growth is the rising prevalence of genetic and rare diseases. Millions of individuals worldwide suffer from conditions that currently have limited or no effective treatments. AAV-based gene therapies offer a promising solution, driving investment in research and manufacturing capabilities.

Technological advancements in large-scale production and purification of AAV vectors are also playing a pivotal role. Innovations in upstream and downstream processing, improved vector design, and enhanced purification techniques are enabling higher yields and better product quality. These advancements are making AAV manufacturing more efficient and cost-effective.

Additionally, the growing trend of outsourcing manufacturing to contract development and manufacturing organizations (CDMOs) is accelerating market expansion. Pharmaceutical and biotechnology companies are increasingly relying on specialized CDMOs to meet the complex requirements of AAV production, ensuring scalability and regulatory compliance.

Segmental Analysis

By Vector Type

The market is segmented into AAV2, AAV5, AAV8, AAV9, Novel Engineered Serotypes, and Others. Among these, AAV2 and AAV9 are widely used due to their established safety and efficacy profiles. AAV9, in particular, is gaining traction for its ability to cross the blood-brain barrier, making it highly suitable for neurological applications. Meanwhile, novel engineered serotypes are emerging as a key growth area, offering improved targeting capabilities and reduced immune response.

By Application

Based on application, the market includes Gene Therapy, Vaccine Development, Research Applications, and Others. Gene therapy dominates the segment, accounting for the largest share due to the increasing number of clinical trials and approved therapies. Vaccine development is also gaining momentum, especially following the global focus on infectious disease preparedness. Research applications continue to support innovation, with academic institutions and biotech firms actively exploring new therapeutic possibilities.

By Disease Indication

The market is categorized into Oncology, Neurology, Ophthalmology, Hematology, Metabolic Disorders, and Others. Neurology and ophthalmology are among the leading segments, driven by the success of AAV-based therapies in treating conditions such as spinal muscular atrophy and inherited retinal diseases. Hematology is also a significant segment, particularly for disorders like hemophilia. Oncology is emerging as a promising area, with ongoing research exploring the use of AAV vectors in cancer treatment.

By Production Method

AAV vector manufacturing involves several production methods, including Transient Transfection, Stable Cell Line, Baculovirus System, Herpes Simplex Virus (HSV) System, and Others. Transient transfection is currently the most widely used method due to its flexibility and scalability in early-stage production. However, stable cell line systems are gaining popularity for large-scale commercial manufacturing, offering consistent yields and reduced variability. Baculovirus and HSV systems are also being explored for their potential to enhance production efficiency.

By End User

The market serves a diverse range of end users, including Pharmaceutical & Biotechnology Companies, Contract Development & Manufacturing Organizations (CDMOs), Academic & Research Institutes, and Others. Pharmaceutical and biotech companies represent the largest segment, driven by increasing investment in gene therapy development. CDMOs are experiencing rapid growth as outsourcing becomes a preferred strategy for managing complex manufacturing processes. Academic and research institutes play a crucial role in early-stage innovation and discovery.

Regional Insights

Geographically, the North American market dominates the AAV vector manufacturing landscape, supported by strong research infrastructure, significant funding, and the presence of leading biotech companies. The United States is at the forefront, with numerous gene therapy trials and commercial manufacturing facilities.

Europe holds a significant share, driven by increasing investments in advanced therapies and supportive regulatory frameworks. Countries such as Germany, the UK, and France are actively contributing to market growth through research initiatives and collaborations.

The Asia-Pacific region is expected to witness the fastest growth during the forecast period. Factors such as expanding biotechnology sectors, increasing healthcare investments, and growing government support for gene therapy research are driving market expansion in countries like China, Japan, and India.

Competitive Landscape

The AAV vector manufacturing market is highly competitive and characterized by rapid innovation and strategic collaborations. Key players are focusing on expanding their manufacturing capabilities, developing advanced vector technologies, and forming partnerships to strengthen their market position.

Companies are investing heavily in capacity expansion and technological advancements to meet the growing demand for AAV vectors. Strategic collaborations between biotech firms, research institutions, and CDMOs are accelerating the development and commercialization of gene therapies.

Market Trends

Several key trends are shaping the future of the AAV vector manufacturing market:

- Shift Toward Scalable Manufacturing: Increasing demand for commercial-scale production is driving the adoption of advanced manufacturing technologies and automation.

- Emergence of Next-Generation Vectors: Novel engineered AAV serotypes are being developed to improve targeting, reduce immunogenicity, and enhance therapeutic outcomes.

- Integration of AI and Data Analytics: Advanced data tools are being used to optimize production processes and improve quality control.

- Growing Role of CDMOs: Outsourcing is becoming a key strategy for companies looking to accelerate development timelines and reduce costs.

- Focus on Regulatory Compliance: Stringent regulatory requirements are driving investments in quality assurance and validation processes.

Challenges

Despite its strong growth potential, the AAV vector manufacturing market faces several challenges. High production costs and complex manufacturing processes remain significant barriers. Additionally, scalability issues and the need for specialized infrastructure can limit market expansion.

Regulatory complexities and the time required for approval of gene therapies also pose challenges. Furthermore, immune responses to AAV vectors and limitations in payload capacity are areas that require ongoing research and innovation.

Future Outlook

The future of the AAV vector manufacturing market is highly promising, with continued advancements expected to address current limitations and unlock new opportunities. As gene therapy becomes more mainstream, the demand for high-quality AAV vectors will continue to rise.

Ongoing research into novel vector designs, improved production methods, and enhanced delivery mechanisms will further drive market growth. The increasing number of approved gene therapies and expanding clinical pipelines will create a strong foundation for sustained expansion.

Note on Competitive Landscape

While this report focuses on the AAV vector manufacturing market, it is important to note that competitive dynamics vary significantly across industries. For instance, the Herbal Products Market is characterized by a broad base of manufacturers such as Himalaya Drug Company, Nature’s Bounty Co., Blackmores Limited, Patanjali Ayurved Limited, and Dabur India Limited, among others. In contrast, the AAV vector manufacturing market is more specialized, with fewer players operating in a highly regulated and technologically intensive environment.

Conclusion

In conclusion, the global AAV vector manufacturing market is set for substantial growth, driven by the rapid advancement of gene therapy and increasing demand for innovative treatments. With a projected CAGR of 13.4% through 2035, the market offers significant opportunities for stakeholders across the biotechnology and pharmaceutical sectors.

As technology continues to evolve and investment in gene therapy increases, AAV vector manufacturing will play a pivotal role in shaping the future of medicine, enabling the development of life-changing therapies for patients worldwide.